The ban on genetic test insurance discrimination

The ability for life insurers to discriminate based on adverse predictive genetic test results will be banned under a new Government proposal.

Predictive genetic tests detect gene variants associated with heritable disorders that appear after birth, often later in life, but are not clinically detectable at the time of testing.

To overcome concerns about discrimination by life insurers, the Government has announced a total ban on predictive genetic testing.

Life insurance and genetic testing

Voluntary insurance, including life insurance is individually underwritten and ‘risk-rated’. The cost of premiums is proportionate to the unique risks of the person seeking the cover. Most of us would be familiar with the questions about family history, personal medical history and habits.

As life insurance is a guaranteed renewable product, once a policy has been underwritten and commenced, the life insurer cannot change or cancel a person’s cover, provided they pay all future premiums when due – premium prices will change across a risk pool, for example based on age. This is why it’s important to carefully assess changing life insurance policies if health issues or conditions have arisen since you put the original policy in place.

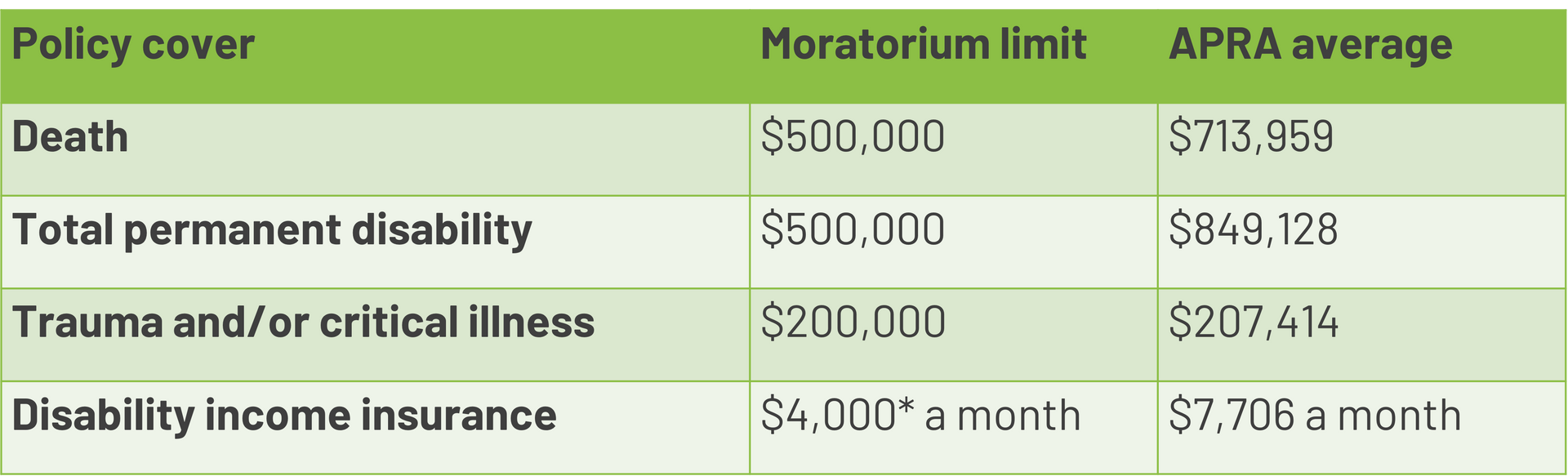

In 2019, Australia’s life insurance industry introduced a partial moratorium on the requirement to disclose genetic test results. The moratorium, which is in place for life insurance applications received from 1 July 2019, prevents genetic results being used for certain types of insurance cover below certain thresholds. However, using APRA data, when compared to the average sum insured, the moratorium coverage thresholds are well below par:

*any combination of income protection, salary continuance or business expenses cover.

Genetic test discrimination

Despite the moratorium, there is evidence that people are not undertaking genetic tests or participating in scientific research because of concerns about obtaining affordable life insurance. And, discrimination still exists.

The Australian Genetics and Life Insurance Moratorium: Monitoring the Effectiveness and Response Report by Monash University found that of the consumers surveyed who had undertaken a genetic test, 35% reported difficulties obtaining life insurance including insurers rejecting life insurance applications, financial advisers advising participants that their applications would be rejected, and insurers placing conditions on insurance policies or charging higher premiums.

Alarmingly, a 43 year old woman with a BRCA2 variant and no personal history of cancer, was denied life cover outright despite having her ovaries and fallopian tubes removed, and regular intensive breast imaging.

The Government response

The Government has stepped in and announced a total ban on the use of genetic testing in life insurance underwriting. The ban will be subject to a 5 year review. However, the Government has not introduced legislation enabling the reforms nor has it announced the date that the ban will take effect.

And, the total ban impacts predictive genetic testing only – it does not cover clinical diagnostic genetic testing to confirm a suspected condition based on signs or symptoms.

A global issue

Australia is not the first country to grapple with the issue of adapting to the increase in available genetic data.

In the UK, insurers cannot use predictive genetic test results unless the result is favourable, or the result has been given to the insurer (voluntarily or accidently). Huntington’s disease is a specific exception for life cover worth more than £500,000.

Canada’s Genetic Non-Discrimination Act prohibits any entity (including insurers) from requesting or using genetic test results. The exception is for individuals to voluntarily disclosure a test result showing they do not have a genetic change that runs in the family.

In the USA, the Genetic Information Nondiscrimination Act (GINA), prevents genetic test results being used in health insurance and employment contexts but not life insurance. The US state of Florida however introduced a law prohibiting life insurers from using predictive genetic test results in underwriting.